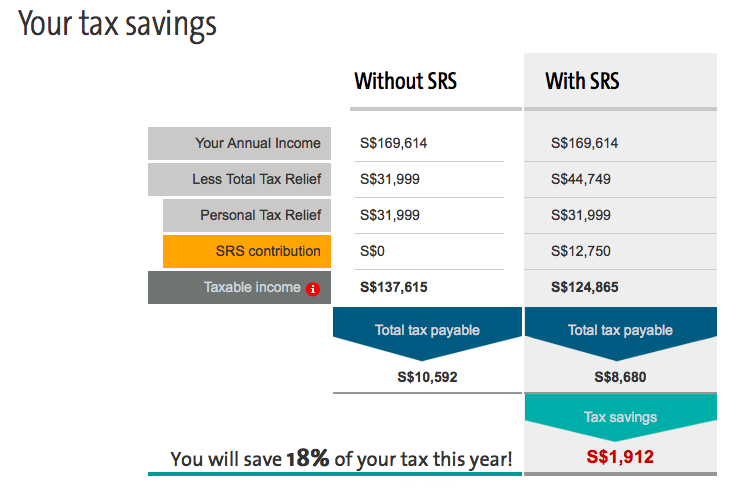

I received a nasty bill in my mailbox last week ! My tax bill crossed 10K SGD mark this year !!! I’ve always read about how Supplementary Retirement Scheme can help reduce Tax but I have never seriously looked at it. Curious, I googled and found the OCBC SRS website OCBC - Supplementary Retirement Scheme. The website comes with a really neat tax savings calculator that claimed that I would be able to save approximately 1.9 K i.e. 18% if I were to contribute a maximum value of 12,750 SGD.

Source : OCBC

Initially, 18% sounded like a really good bargain. However, there are a set of conditions that I need to comply to. If I decide to withdraw this money earlier, the amount withdrawn is subjected to tax and 5% penalty. If I were to withdraw this amount at or after 62 years old, only 50% of the withdrawn amount is subject to tax. Interest is only at 0.05% p.a on the cash balance in the SRS account but I am allowed to make investment on this account.

To be honest, I think it’s a bad deal. My tax assessment this year already includes the 12,750 SGD that I am planning to contribute to SRS. Thus, to enjoy a tax savings of 18%. I need to lock up my capital and subject myself to another round of taxation when I am at or after 62 on this same amount. Yet, the interest is only at a pathetic 0.05% p.a. unless I actively invest this amount.

Hmm…what is your experience with SRS ? Do you think it’s a good bargain? Any other ideas to save tax? I am all ears :-).

Hmmm…as singles, not much tax reliefs we can get. So, I think having this deferred tax program is better than nothing at all. I’m not too keen to give so much money as taxes since on a day to day basis, I’m already contributing 7% gst. My taxes this year is almost my 1 month salary. So, I even started to contribute to cpf min sum top up to reduce tax next year.

I have some high dividend yield stocks in SRS which gives me decent return. And I’m satisfied. 🙂

Hi PF,

Topping up CPF min sum sounds like a great plan :). Thanks for sharing.

You can withdraw when you get retrenched during your career. That means your income tax bracket for the withdrawn amount is lower.

the savings is lesser 18%-5% maybe. But still worth it. If you are investing your srs in stocks, you can consciously determine that to be your retirement sum. If you withdraw less than 30k a year when you are retired, the tax savings is maximum.

You can consider voluntary contribution to your cpf up to 30600 also. Part of it goes to oa which you can buy house. Use the medisave acc to buy medical insurance for parents.

Hi NoName,

If I withdraw when I get retrenched, I will face a penalty of 5% and taxed 100% for the income withdrawn if I am not wrong. Voluntary contribution to CPF sounds like a plan ;-). Thanks for sharing.

You can further reduce your taxes by sharing your wealth with the less fortunate of your choice.

This contribution to the less fortunate is multiplied by 2.5 times to reduce your taxable amount. 😀

Topping up parents cpf account also helps to lower your tax contribution. 🙂

Hi Numbers,

Kool ! Guess it’s a reminder for me to start opening up my heart to the less fortunate :-). Not sure whether my parents would be too happy when I announce to them that they would no longer be getting allowance in cash from me, but through CPF. Worth a try I guess as it gels well with the cpf lifetime min sum benefits they would enjoy. Thanks for sharing.

You can consider giving some money to charity. Every $1 you donate will give you 2.5 times relief. So a $10,000 donation effectively can reduce your taxable income by $25,000.00. You can do charity while reducing your tax bill in the mean time.

Hi Vincent,

Charity ! What a great idea! Will include this in my coming new year resolution :-). Thanks for sharing.

Hi Lady,

You will only be taxed on withdrawing monies from the SRS account after 62 if the amount you withdraw exceeds $40,000 a year. Even if you withdrew $60,000 a year, you will only pay taxes on $10,000 at the 2% rate, which is just $200.

As long as you plan to retire before 62 and have enough money to cushion you through any hard times until 62, I think the SRS is extremely good.

If you plan to work in a similar capacity as currently past the age of 62, you will still have to pay a high income tax, so it does not really help you much.

I think the SRS account is very good only if you know that the money you set aside in it will not be needed anytime soon, and you wish to grow your retirement nest egg even bigger and faster.

I have wrote about the SRS before, maybe my post might be useful to you: http://gotmoneygothoney.blogspot.sg/2014/04/supplementary-retirement-scheme-srs-and.html

Cheers,

MH

Hi MH,

Thanks for sharing. Great Insights !

Dear lady, I’m not sure abt volunteer cpf top up. There is a cap of how much u can contribute per year, I think. And that cap minus away ur contribution from your job is the max u can do voluntary contribution. This one I am not sure. Pls research and confirm.

Cpf min sum top up is direct to the Cpf-SA. Provided the SA plus MA is less than the prevailing min sum. If u already met min sum, then u can’t do this top up anymore. And even if u can, its just 7k tax relief max. SRS is 12,750.

I’m contributing for both. Did a tax projection next yr. Hopefully I can contain my taxes to 1mth of my salary or below.

Hi PF,

Thanks for clarifying. Looks like I need to do some math and googling here :). You are doing great in “escaping” tax :-).

I posted on this subject before. Info may be a bit dated. Perhaps useful.

http://lizardorealm.blogspot.sg/2010/08/maximising-returns-with-minimal-risks.html

With the tax avoidance savings, consider if you were to take the same savings to donate. And as mentioned in an earlier comment, this gains a further deductible at 2.5x the donation. At the 18% tax bracket, every $4,000 donated actually generates $10,000 in deductible. That’s a further $1,800 of tax avoided. So in truth, you would only need to spend $2,200 for that $4,000 donation.

Hi Lizardo,

I love this donation idea ! :-). Thanks for making the math clearer. Am getting rusty with numbers with all these t&cs.

Take that $12,750 and invest. Can buy Unit Trust and Stocks as per usual.

If you were to subsequently withdraw post-retirement $40,000 per year over 10 years, you would pay no tax – assuming (a) no other taxable income, (b) the policy remains that only half of the SRS sum withdrawn is taxable, (c) that it remains that for taxable income below $20,000, no taxes are levied.

Hi Lizardo,

Thanks for the input. There’s so much t&cs when one reaches 62 – 65 in Singapore. Tax, how much to withdraw, how much to keep as CPF min sum, Medishield, Eldershield etc…Sigh, really needs to pray one doesn’t get dementia or alzheimer :-). Feels like retiring is a full time job, rather than a time for celebration !!

Already not too bad. Try understanding the US, UK or Aussie systems!

And so true about not getting any of those touch wood problems. It will be so difficult to manage if any of those happen.

Hi Lizardo,

Agree !! Touch wood 🙂

Seems like no one mention tax on capital gain…. That is if your srs ROI is fantastic and the after 62 withdrawal is not managed properly, you may end up paying more tax ie capital gain tax.

Hi Jimmy,

Thanks for highlighting !! This was on my mind as well. I wonder if I made a stock investment that pays dividends. Typically, the tax would be deducted before it is returned to the SRS. When I reach 62, how do they know which amount has already been tax deducted and which are not. Any idea?

They dun, so double tax. And if the retirement age is raised (probably will), we will have a shorter window to withdraw and enjoy our retirement.

Hi Jimmy,

Wah, looks like topping up CPF min sum is a better plan than topping up SRS. At least there’s no tax on CPF withdrawal and whatever capital gain on investment.

Yeah…it takes a lot of planning to retire! Although I think I won’t retire.

I’ve been studying ways to plan my taxes when I realized that this year we hv no discount from govt per last 2 yrs….sigh. I’ve also started to donate to sg charities for tax relief. I used to donate to World Vision. Now my choice charities this year are ST school pocket money fund and children’s society where ocbc donate 1 for every 2 bucks I donate.

Hi PF,

I need to start thinking like you. Stop thinking about Retiring :). Hahaha

Any tips on how to go about hunting for charities to donate? Is there a blessed list of charity organizations recognized by the IRAS?

Yes, there is a list. U can do a search on Iras. 🙂

Hi pf,

Thanks!! Found it, here’s the link http://www.iras.gov.sg/irasHome/page04.aspx?id=1268.

Btw, thanks to all the ppl who comment, I learnt something new too. Abt taxation on capital gains for SRS, etc. But actually, if u think abt it. ..this money is for old age and in the event we lost our jobs, so govt also thought abt deterring us from using this money for speculation and high risk-high yield investments. Which means, its really a guided approach for this SRS.

For me, I more or less have a portfolio approach to manage my money. Money for retirement is subject to little risks. More about preservation.

Money for capital growth is largely short to mid term horizon. Subjected to more risks.

So, I don’t think there is an absolute yes or no to SRS. Depends on how you manage your portfolio. Also depends on how savvy you are as an investor. If you do very well, then its not that beneficial to you. But who can say they always make the right investment decisions?

I’m the type that squirrels away bits of money here and there so that I forgot abt them or can’t touch them and can’t spend them.

Afterall I guess everybody needs to know themselves well to choose their path. 😀

Hi pf,

Agree, my readers are all so savvy! Really appreciate the generous contribution from all the readers above :-). A BIG THANK YOU to all !!!

Hi All,

I think there is a misconception about capital gains tax. There is no capital gains tax for shares in Singapore. (source: http://www.iras.gov.sg/irashome/page04.aspx?id=152 )

When withdrawing from your SRS account past age 62, 50% of the withdrawal amount will be taxed as income. If you have no current income (assuming you are now retired), you can withdraw up to $40,000 tax free, since only 50% of the withdrawn amount is taxed, and income up to $20,000 is free. (see pt. 44, source: http://app.mof.gov.sg/data/cmsresource/srs/SRS_Booklet%20-%2018Feb11.pdf )

Therefore it really is very beneficial to grow your retirement funds in the SRS up to, but not beyond, the $400,000 mark. Then an optimum amount of $40,000 can be withdrawn every year tax free over the next 10 years.

MH

Hi MH,

Thanks for highlighting. Let me go do some serious digging with IRAS 🙂

A bit confused. Capital gain & dividend are taxable for SRS account? Although I tend to agree with MH that it’s not true.

I studied this before too, I think the only factor to consider is property. Because SRS can’t be used to buy property, so if you need the money as down payment, then must think carefully.

The good thing is SRS can be used as emergency fund if suffer long time unemployment, withdraw the money to cover daily expense without tax.

Hi Ah John,

If you suffer long time employment and you withdraw the money before 62, you will be tax 100% and incur a penalty of 5% if I am not wrong ?! Of course, you probably assume that you will not withdraw a huge amount of money in one go during the unemployment phase.

CPF top-up only goes to SA, can we invest SA money? Also it can’t be withdrawn earlier.

Hi John,

4% interest on SA money is pretty decent. 🙂

I think the idea for “capital gains tax” is what if one is very successful at investing with the SRS and the balance inside is more than 400k. Then in the end, we might withdraw more than 40k per year if the 10year period to withdraw it is fixed. Then ultimately, what we may withdraw is not what we put in but the capitals gains portion which might get us taxed.

Hi pf, MH and Ah John,

I called up IRAS to clarify on whether dividends and capital gains from shares investment in SRS shall be taxable at 62 upon withdrawal.

Their answer is yes. Thus, although dividends and capital gains from shares may not be taxable in normal cases (source: http://www.iras.gov.sg/irashome/page04.aspx?id=152 ). If it gets into SRS, it will be subjected to tax at 62 upon withdrawal, unless you regulate the amount you withdraw per year. Hope this helps!

I guess this is a deterrent for us to take huge risks in investments with our SRS for capital gains. Anyway, since we already deferred the taxes for so many years, by that time even if we r taxed a bit for it, also ok bah.

….nation building mah. 😀

Hi PF,

Hahaha… I love your positive thinking :).

Hahaha…I mean, come on…if we r drilling into this matter in such detail, we r all earning good money. 😀

When I had my first job, my pay was $1,300. There were not many choices in all things, all aspects. Looking back, life was much simpler. Happier in some ways. Haha… 🙂

Hi pf,

So true :-). The good old simpler days ….

Hi Lady,

What about topping up your parents CPF?

Hi HokkienPeng,

Good Idea :).

Hi Lady,

You can make donation to universities to get the most value out

– you get 2.5x tax relief of your donation amount

– Government also matches 1:1 of your donation to the school

e.g. you donate $100, and your tax rate is 20%, you get $100×2.5*20%=50 tax relief. So effectively, you just donate 50$. On the university side, they got $200 donation from you and the government.

Hi Ian,

Thanks for the tip :). I didn’t know we can also donate to universities. I wished when we declare our tax, there is a checkbox where we can tick where we want to make our donations and the amount we want to donate to and it is deducted directly from the tax invoice and transferred to the relevant communities accordingly.

Your donation needs to go into the beneficiary before end of income assessment year to enjoy tax relief. You need to approach community separately for donation, I like it this way as it promotes accountability of individual communities for obtaining donations.

Hi Ian,

Interesting view. I would rather these individual communities focus on executing the task they were meant to do than to spend time and $$$ trying to market themselves in order to garner donations.

Pingback: What does progressive income tax means to Singaporeans | A WordPress Site